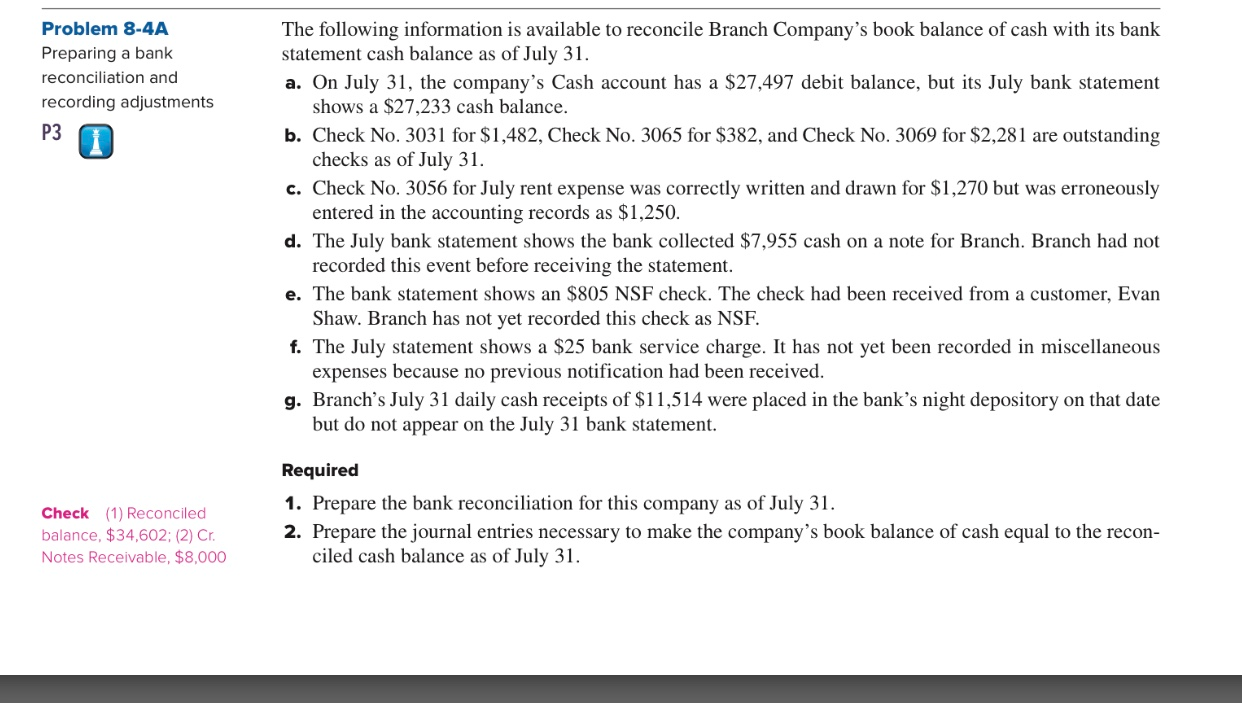

(11) 95720-0227

There are reasons for depending loans designed to LMI census tracts once the qualifying to have CRA conformity

In many cases, money info is shed out of this research. I’ve assigned destroyed viewpoints proportionately within groups. Actually, the study from mediocre mortgage proportions revealed for the table step three reveals that the destroyed viewpoints be a little more likely to be money in order to high-earnings individuals, so the study inside the dining table 2 may actually overstate the brand new LMI debtor show.

Not merely is geography the fresh historic base of your own CRA, however, such as for instance financing prompts money range in low income tracts. However, 60 percent of your dollar worth of finance for the LMI census tracts is not going to LMI consumers.

You to definitely iners should look on personal lender conclusion to make sure individual institutions are not extremely depending on this version of lending to satisfy the CRA duties

Which is, examiners should make sure one to associations aren’t only skimming the new huge, more lucrative finance when you look at the gentrifying areas to count towards the CRA criteria.

Furthermore, when considering CRA modernization, this studies enhances the matter of whether one to would like to membership for the pattern here’s giving less CRA credit to have loans to better earnings borrowers when https://elitecashadvance.com/installment-loans-oh/ you look at the lower income elements.

Listen and signup now.

The new Metropolitan Institute podcast, Evidence doing his thing, inspires changemakers to lead having facts and act that have collateral. Cohosted by Metropolitan Chairman Sarah Rosen Wartell and you can Executive Vp Kimberlyn Leary, the occurrence keeps inside the-depth discussions that have professionals and you can leadership with the subject areas ranging from exactly how to progress guarantee, to developing innovative choice one to reach people impact, to what it means to apply evidence-mainly based leadership.

Congress enacted the fresh new 1977 Neighborhood Reinvestment Work (CRA) to help you remind depository organizations to greatly help see the communities’ credit needs, like the means from lower- and you will average-income (LMI) neighborhoods. On the , 25 years after the past major upgrade for the laws, the office of Comptroller of one’s Currency (OCC) awarded this new laws and regulations who would significantly alter the system to own comparing banks’ CRA results

Although the financial world has substantially altered due to the fact CRA are passed, the present day laws work relatively really. One modernization perform is going to be rooted in analysis, and you may, as we wrote in other places, you do not have having change in the middle of an excellent pandemic.

Perfect research one to teach the most recent regulations are working is also offer a critical basis to possess modernization. Capable show us in which and just how CRA credit is produced and whether or not and just how the fresh new CRA was helping all the teams (as well as LMI neighborhoods) where for each and every bank operates.

To construct evidence legs, we reviewed 2018 analysis in regards to the amount of CRA credit financial institutions engaged in for every of your four big mortgage groups: single-family relations mortgages, home business loans, short ranch money, multifamily funds, and you will area development finance. (The methodology is explained lower than.) This can be an improve in order to an analysis we did playing with 2016 studies. The email address details are revealed into the dining table step 1.

- People development and you may single loved ones financing switched metropolitan areas during the 2018 while the adding the very best quantity of CRA borrowing from the bank, that have people development lending swinging off 2nd input 2016 with $96 billion within the credit in order to first place into the 2018 which have $103 million.

- Single-family relations financing frequency fell significantly, off $108 mil in 2016 in order to $95 billion within the 2018, a result of the fresh new reduced total of re-finance frequency between them ages.

- Even though the acquisition of one’s almost every other about three version of financing stayed a similar within the 2018, the fresh new multifamily CRA sum rose notably, out of $33 million so you’re able to $42 billion, together with share off small company and you will brief ranch fund decrease some, to $86 billion and you will $8 mil respectively.